Match Day & Physician Relocation Timeline

Jessica Hegge

TLDR

\\Match Day, a new fellowship, or a first attending position often means relocating on a tight timeline. Buying a home before you have set foot in your new city, sometimes before your first paycheck, can feel daunting. Physician mortgage programs are built for exactly this scenario, and a clear timeline makes it manageable.

Dr. Home Finance is a research and matching service, not a lender. We connect relocating doctors with banks that run physician programs so you can line up financing around your move.

Why physician programs fit relocation

The standout feature for relocating doctors is the ability to qualify on a signed employment contract before your start date. Many lenders allow closing with a start date a defined window in the future, which means you can buy a home before your new job begins. Our eligibility and qualifying guide covers how the contract-based approach works.

A home-buying timeline for newly matched doctors

While every situation differs, a typical timeline looks like this:

3 to 4 months out: Get pre-approved. Compare physician programs and understand what you can borrow. Get matched with lenders early so you are ready to move when you find a home.

2 to 3 months out: Connect with a local realtor who knows your new market and start shopping, in person or virtually. Decide whether to buy now or rent first.

1 to 2 months out: Make an offer, go under contract, and begin underwriting. Provide your signed employment contract and other documentation.

Move-in: Close on the home, ideally timed near your start date within the lender's allowed window.

Use our physician mortgage calculator to ground your budget before you shop, and review Physician Mortgage 101 for the fundamentals.

Buying before you start using your contract

To buy before your first paycheck, you generally need a fully executed employment contract with a clear start date and compensation. The lender uses this as proof of future income. Confirm each lender's allowed window between closing and start date, since it varies. Have your contract, identification, and financial documents ready to keep underwriting moving.

Moving across state lines

Relocating to a new state adds a few considerations:

Program availability varies by state. Not every lender operates in every state, and terms can differ. Browse options in your destination, for example Florida, Texas, or California, to see what is available.

Local expertise matters. A realtor and banker who know your specific market help you avoid surprises on pricing, taxes, and neighborhoods.

Rent vs buy. If you are unsure about the area or your tenure, renting first is a reasonable choice. Buying makes more sense when you expect to stay several years.

Should you buy or rent first?

Buying immediately is not always the right call. Consider renting first if you are unfamiliar with the city, your position might be short-term, or you want time to learn the market. Consider buying if you expect to stay, have found a home that fits, and the numbers work. The decision is personal, and a banker who works with physicians can help you weigh it.

What to do if you don't match

Not matching is stressful, and it changes your housing plans. If you are entering the SOAP process or reapplying, hold off on a home purchase until your position and location are settled. There is no rush to buy without a confirmed contract and start date. Once your path is clear, the same physician programs will be available to you. Renting in the interim preserves flexibility while you finalize your next step.

Frequently asked questions

Can I buy a home before I start my new job?

Yes. Many physician programs let you qualify on a signed employment contract and close before your start date, within the lender's allowed window.

How early should I start the process?

Starting pre-approval around three to four months before your move gives you room to compare programs and shop without rushing.

What if my new job is in another state?

Program availability and terms vary by state. Review options in your destination market and work with a local realtor and banker.

What if I don't match?

Wait until you have a confirmed position and start date before buying. Renting in the meantime keeps your options open, and physician programs will still be there when you are ready.

Plan your move with the right financing

A relocation goes more smoothly when financing is lined up early. Get matched with lenders that run physician programs and see your options in your new market.

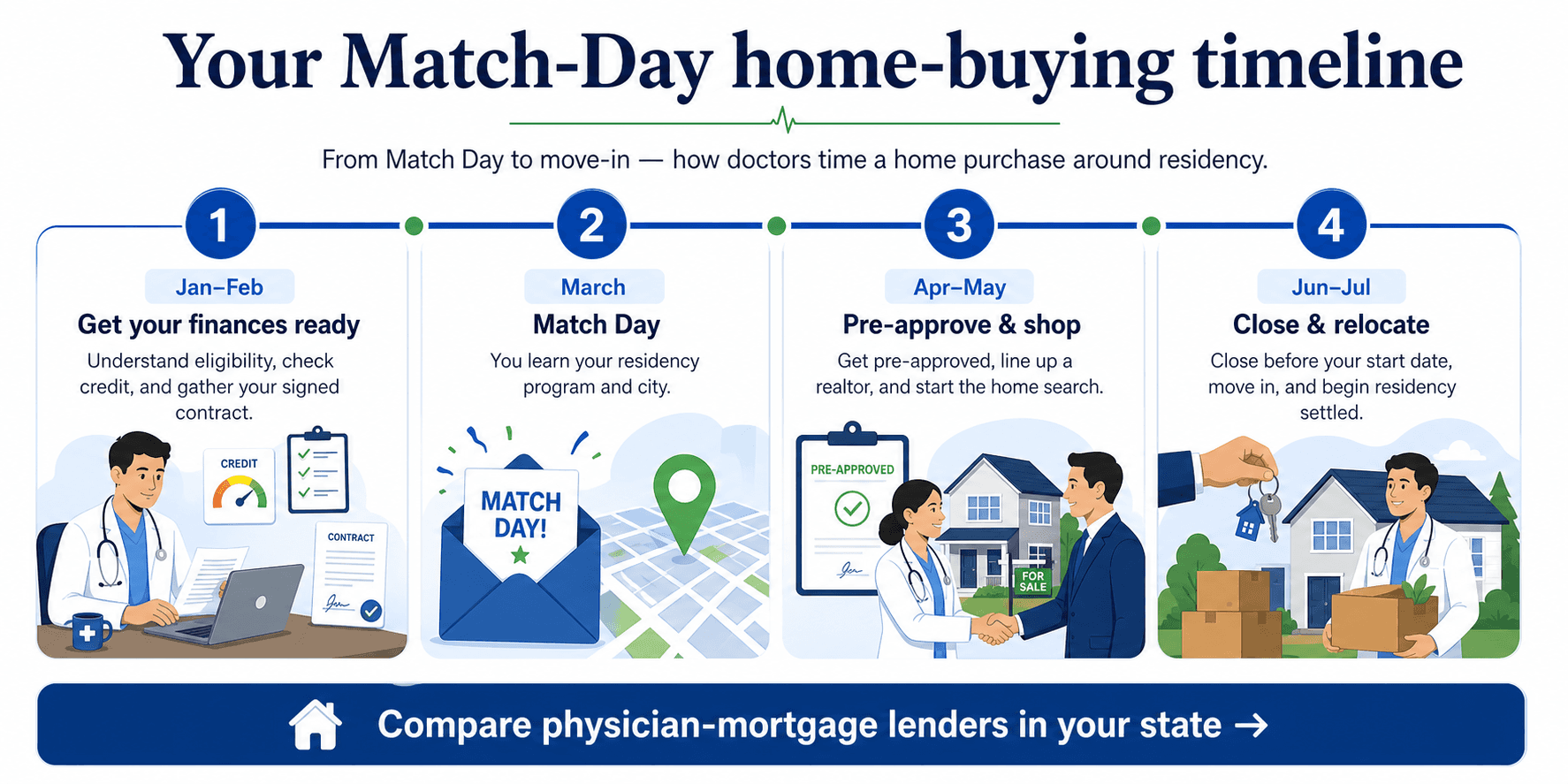

Your Match Day home-buying timeline

Match Day falls on the third Friday of March (March 20 in 2026), and most residencies begin in late June or early July. That compresses the entire relocation and home purchase into a roughly four to six month window. Here is how the peak January to July season tends to unfold.

January to February: get your finances ready

Pull your credit, review your student-loan situation, and gather recent financial documents.

Learn how physician-mortgage eligibility works so you know what to expect once you have a contract. Our eligibility and qualifying guide walks through the basics.

March: Match Day

On Match Day you learn your program and city. This is the moment your destination, and therefore your housing search, becomes real.

Start researching neighborhoods and begin comparing physician programs available in your new state.

April to May: pre-approval and the home search

Once you have a signed employment contract, get pre-approved on that contract and define a realistic budget.

Line up a physician-savvy local realtor and begin the home search in earnest, in person or virtually.

June to July: close and relocate

Go under contract, complete underwriting, and aim to close before your start date within the lender's allowed window.

Move in and settle before orientation begins so you can focus on your new role.

Starting early in this window keeps the timeline calm rather than rushed. Get matched with lenders that run physician programs in your destination state.

Related guides

Compare physician‑mortgage lenders in your state →

Reviewed by Jessica Hegge, Partner at Dr. Home Finance · Our editorial process · Last reviewed July 2026. Dr. Home Finance is a research and matching service, not a lender or broker; all loan terms are provided by third-party lenders and subject to their approval. Equal Housing Opportunity.

Get matched with a physician mortgage lender